IndusInd Bank’s shares witnessed a sharp decline, crashing below the ₹700 mark, after the bank reported a significant impact on its net worth due to discrepancies in its derivative portfolio.

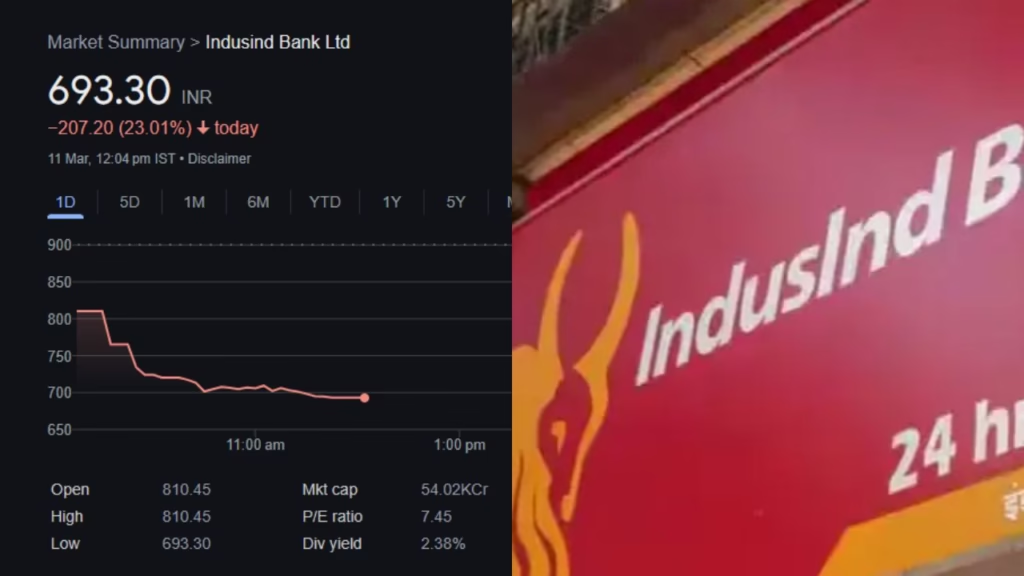

IndusInd Bank’s share price took a dramatic nosedive, crashing below the ₹700 mark and hitting a 52-week low. This steep decline was triggered by the bank’s alarming disclosure of discrepancies in its derivative portfolio, projecting a 2.35% hit to its net worth—equivalent to roughly ₹1,530 crore to ₹2,100 crore. The news sent shockwaves through the market, erasing over ₹14,000 crore in market value in a single day and raising serious questions about the bank’s financial health and credibility.

The financial world was abuzz as IndusInd Bank, one of India’s prominent private lenders, revealed this unsettling development in a regulatory filing late on March 9, 2025. The bank’s internal review, prompted by the Reserve Bank of India’s (RBI) tightened guidelines on investment portfolios issued in September 2023, uncovered accounting irregularities in its derivative transactions spanning the past five to seven years. These discrepancies, tied to forex hedges and internal swap trades halted after April 1, 2024, have cast a shadow over the bank’s operations, leadership stability, and investor confidence. As the stock plummeted 20% to ₹720.35 on the NSE by early trade on March 11, analysts scrambled to reassess their outlook, with several brokerages slashing target prices and downgrading ratings.

This wasn’t just a one-off stumble for IndusInd Bank. The past few months have been tumultuous, marked by a series of red flags: a 39% drop in Q3 net profit to ₹1,402.3 crore, the abrupt resignation of its Chief Financial Officer (CFO) before the December quarter results, and the RBI’s decision to grant only a one-year extension to CEO Sumant Kathpalia instead of the customary three. Now, with the derivative portfolio fiasco unfolding, the bank faces a credibility crisis that could take months—or even years—to recover from. Investors, already jittery from a 50% decline in the stock over the past six months, are left wondering whether this is a temporary blip or a sign of deeper systemic issues.

The root of the problem lies in how IndusInd Bank managed its derivative portfolio, particularly its forex hedges tied to global deposits and borrowings. According to the bank’s filing, the discrepancies emerged during a review of its “Other Asset and Other Liability” accounts, conducted in line with RBI’s Master Directions effective from April 2024. These guidelines prohibited internal trades and hedging practices that banks had previously relied on, forcing IndusInd to scrutinize its books. What they found was a process flaw—specifically, an understatement of costs in inter-desk swap accounting—that had gone unnoticed for years. CEO Kathpalia, addressing analysts on March 10, admitted that the issue was identified between September and October 2024, following the RBI’s regulatory nudge.

The financial impact is staggering. The bank estimates pre-tax losses of ₹2,100 crore, translating to a post-tax hit of approximately ₹1,580 crore, or 2.35% of its net worth of ₹65,102 crore as of December 2024. This one-time charge, which IndusInd plans to absorb through its profit-and-loss account in Q4 FY25, could push the bank into a quarterly loss, especially when coupled with accelerated provisions for its stressed microfinance (MFI) portfolio. While the bank insists its profitability and capital adequacy remain robust enough to weather this storm, the market’s reaction tells a different story. Shares locked at the lower circuit on March 11, reflecting a loss of faith that may not be easily regained.

Brokerages wasted no time in responding. Nuvama Institutional Equities downgraded IndusInd from “Hold” to “Reduce,” slashing its target price to ₹750 from ₹1,115, citing a “discomforting timeline” of events: the CFO’s exit, the CEO’s curtailed tenure, and now this derivatives-induced dislocation. Emkay Global followed suit, cutting its target to ₹875 from ₹1,125 and downgrading to “Add” from “Buy,” warning of near-term pressure due to both the disclosure and ongoing MFI stress. Kotak Institutional Equities took an even harsher stance, reducing its target to ₹850 from ₹1,400 and shifting to a “Reduce” rating, emphasizing the blow to credibility over the relatively modest financial hit. Meanwhile, Morgan Stanley maintained an “Equal-weight” rating with a ₹900 target, acknowledging reduced visibility on the stock’s future.

Analysts point to a broader narrative of governance and oversight concerns. The derivatives discrepancies, though quantified, remain murky in detail. IndusInd has appointed an external auditor to validate its internal findings, with a report expected by the end of March 2025. Kathpalia assured stakeholders that the external review’s numbers should align closely with the bank’s estimates, but the lack of transparency about the nature of these trades—executed over half a decade—has fueled speculation. Was this a case of deliberate mismanagement, or simply a failure to adapt to new accounting norms? The RBI, already aware of the issue, may have factored it into its decision to limit Kathpalia’s extension, signaling discomfort with the bank’s leadership.

For investors, the timing couldn’t be worse. IndusInd Bank was already grappling with headwinds: a slowdown in loan growth, elevated slippages in its unsecured credit segment, and a contracting net interest margin (NIM) amid rising funding costs. The stock, which traded at ₹1,500 levels a year ago, had already shed 42% of its value over the past 12 months. Now, at ₹720.50, it’s down 53% from its peak, making it one of the worst performers among Indian banking stocks. Technical analysts on platforms like X suggest a further slide to ₹750, a key support level, with a breach potentially opening the door to a “major downside.”

Yet, amidst the gloom, there’s a sliver of optimism. IndusInd has emphasized its strong capital buffers and a history of weathering crises. Its deposit growth, particularly in the NRI segment (up 39% YoY to ₹58,600 crore in Q3 FY25), remains a bright spot. The bank’s board is reportedly fast-tracking the search for Kathpalia’s successor, which could restore some stability. Motilal Oswal, maintaining a “Neutral” rating with a ₹925 target, believes a smooth leadership transition might bolster investor confidence over time. However, the consensus is clear: trust, once broken, is hard to rebuild, and IndusInd faces an uphill battle to prove its resilience.

The fallout extends beyond numbers. This episode underscores the risks lurking in complex financial instruments like derivatives, especially when regulatory scrutiny intensifies. For IndusInd, a bank that prides itself on a diverse portfolio spanning retail, corporate, and microfinance lending, the revelation is a stark reminder of the importance of robust internal controls. Competitors like HDFC Bank and ICICI Bank, which have avoided similar pitfalls, may gain an edge as investors seek safer bets in a volatile market.

As March 11 unfolded, social media platforms like X buzzed with reactions. Traders warned of a “house built on sand,” while others speculated about systemic risks in India’s banking sector. The stock’s 20% crash wasn’t just a number—it was a loud alarm bell, signaling that all is not well at IndusInd Bank. Whether this is a temporary setback or the beginning of a prolonged decline hinges on the external audit’s findings and the bank’s ability to restore faith. For now, shareholders are left holding their breath, watching a once-promising lender fight to regain its footing in an unforgiving market.

IndusInd Bank’s share price crash below ₹700 is a stark reminder of the challenges facing the banking sector and the potential pitfalls of complex financial instruments like derivatives. While the immediate impact has been severe, the long-term consequences will depend on how effectively the bank addresses the issue and restores investor confidence.

For now, stakeholders must brace for further volatility and keep a close watch on developments. As the situation unfolds, the lessons learned from this episode will undoubtedly shape the future of risk management in the banking industry.